Credit Scoring: How does it work

When you’re looking to get a loan, lenders usually look at your credit score to see if they should loan to you or not. Even when it’s for a small amount, having your credit score checked can be a nerve-wracking experience, especially when you’re in a variable financial situation.

But what exactly is your credit score? And how is it worked out? In this article, we take an in-depth look at credit scoring, explaining who does it, how it’s done and why it doesn’t always tell the whole story

Who calculates your credit score?

There are several credit reporting agencies in Australia that calculate your score. Equifax, Experian and Illion are among the best known and most widely used agencies in the country. Depending on which agency you use, your score will either be between 0 and 1000 or between 0 and 1200. Your score will fall within a five point scale, ranging from below average to excellent. In basic terms, a high credit score indicates a low risk, while a low score indicates a high risk.

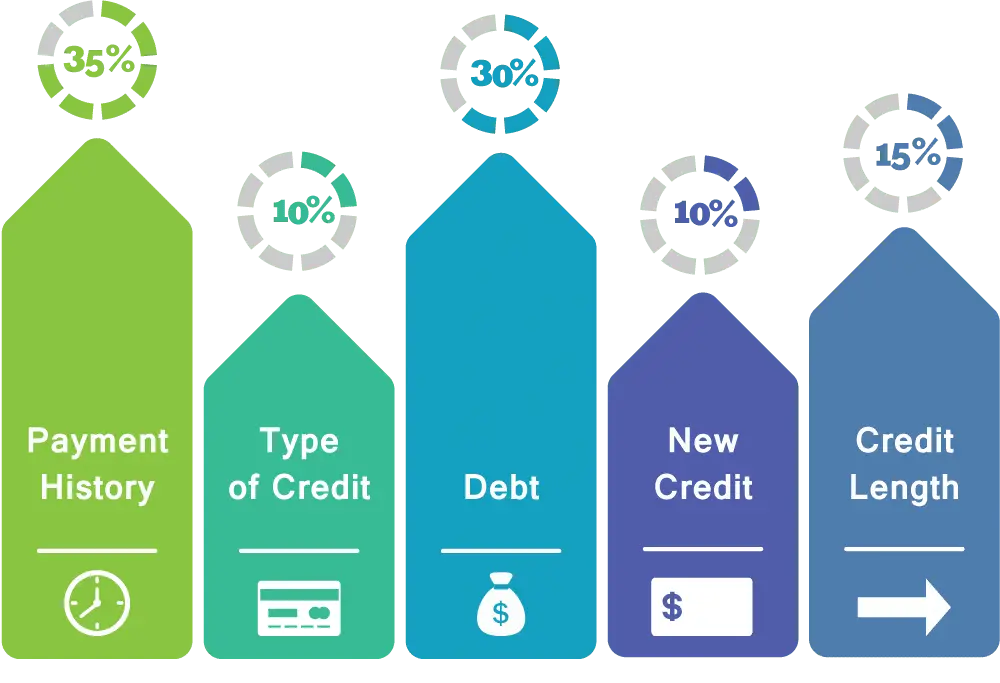

How is your score calculated?

Credit reporting agencies collect your financial and personal information, which is documented on your credit report. Your credit score is based on this information, which includes:

- Your personal details – The credit agencies consider several personal factors, including your age, length of employment and how long you’ve been living at your current address.

- Credit providers you have used – The type of credit provider you have used, or has made an enquiry on your behalf, affects your score. This is because there are different levels or risk associated with different credit providers. For example, the level of risk associated with a bank may be different than that associated with a hire-purchase company or a utility provider.

- The amount of credit you have borrowed – The size of the loan or credit limit you have applied for affects your score.

- The number of credit applications you have made – Each time you make a credit enquiry it’s noted on your credit report, including any mortgage, utilities or other loan enquiries. If you ‘shop around’, enquiring with numerous providers over a short period it will usually negatively affect your score.

- Unpaid or overdue loans or credit – To put it shortly, unpaid debt does not look good on your credit report. If there is default information in your report, such as overdue debts or credit infringements, it will negatively affect your score. Conversely, if there is no default information on record, it will positively affect your score.

- Court writs and default judgements – If you have a court writ or default judgment on your report, it indicates an increased level of risk and will negatively affect your score.

Does my credit score matter?

Yes and no. For many lenders, your credit score matters more than it does for others, who may prefer to look at what’s in your credit report, which your score is based upon. You also need to keep in mind that your credit score does not necessarily tell your whole story – you may easily be able to pay off a loan even though your score suggests otherwise. That’s why some lenders, including Direct Credit, prefer to use alternative lending criteria to determine whether you’re able to pay a loan off or not.